WIFO-Konjunkturtest

Part of the Joint Harmonised EU Programme

of Business and Consumer Surveys

WIFO-Konjunkturtest

Part of the Joint Harmonised EU Programme

of Business and Consumer Surveys

WIFO-Konjunkturampel (economic traffic light)

The results of the WIFO-Konjunkturtest for June show that business sentiment has remained flat. Sentiment continues to be skeptical due to the war in Iran. The WIFO Business Climate Index stood at –5.0 points (seasonally adjusted), 0.1 points below the May figure. Assessments of the current situation deteriorated slightly compared to the previous month (–0.3 points) and stood at –3.8 points, in the skeptical range. Economic expectations improved slightly (+0.3 points) but remained below the zero line at –6.3 points. The price effects and uncertainties stemming from the war in Iran are weighing particularly heavily on manufacturing and retail trade. In the services sector, expectations remain skeptical despite an improvement. The construction industry is showing a decline in current conditions assessments.

Economic Sentiment picks up in both the EU and the euro area, Employment Expectations down in both regions

In June 2026, the Economic Sentiment Indicator (ESI) increased noticeably in both the EU and the euro area (+1.3 points in both areas, to 95.1 points in the EU and 95.0 points in the EA). By contrast, the Employment Expectations Indicator (EEI) fell markedly in both areas (EU: –2.3 points to 92.9 points, euro area: –2.2 points to 92.2 points). Both indicators remain below their long-term average of 100.

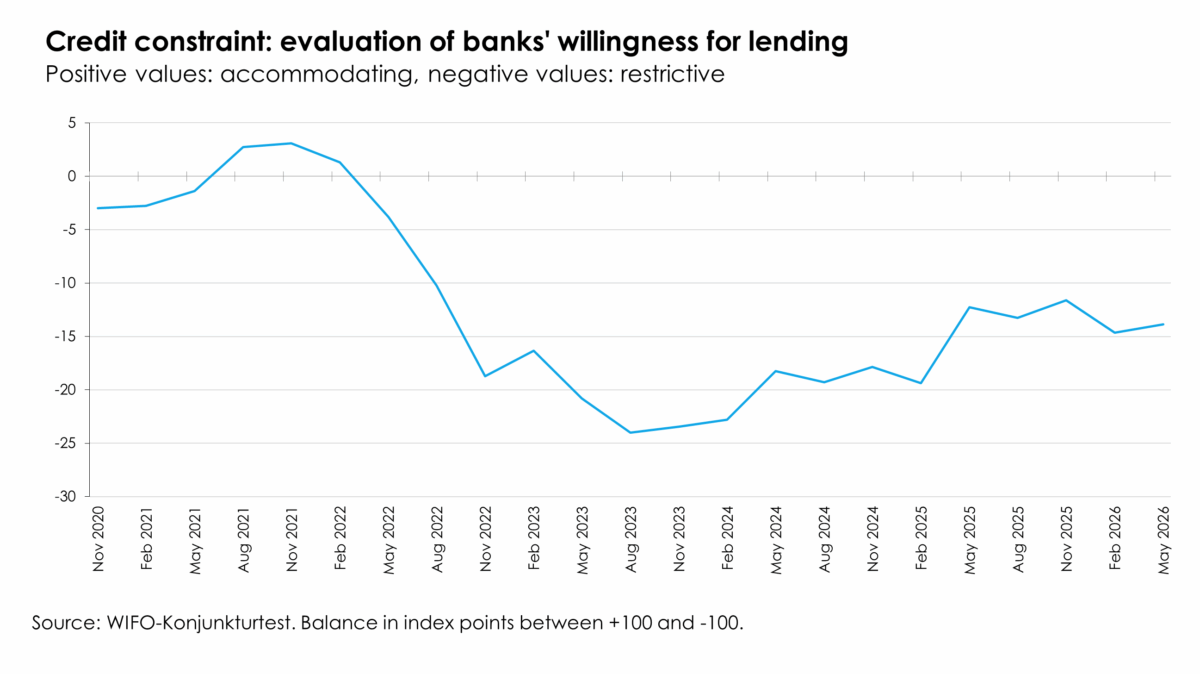

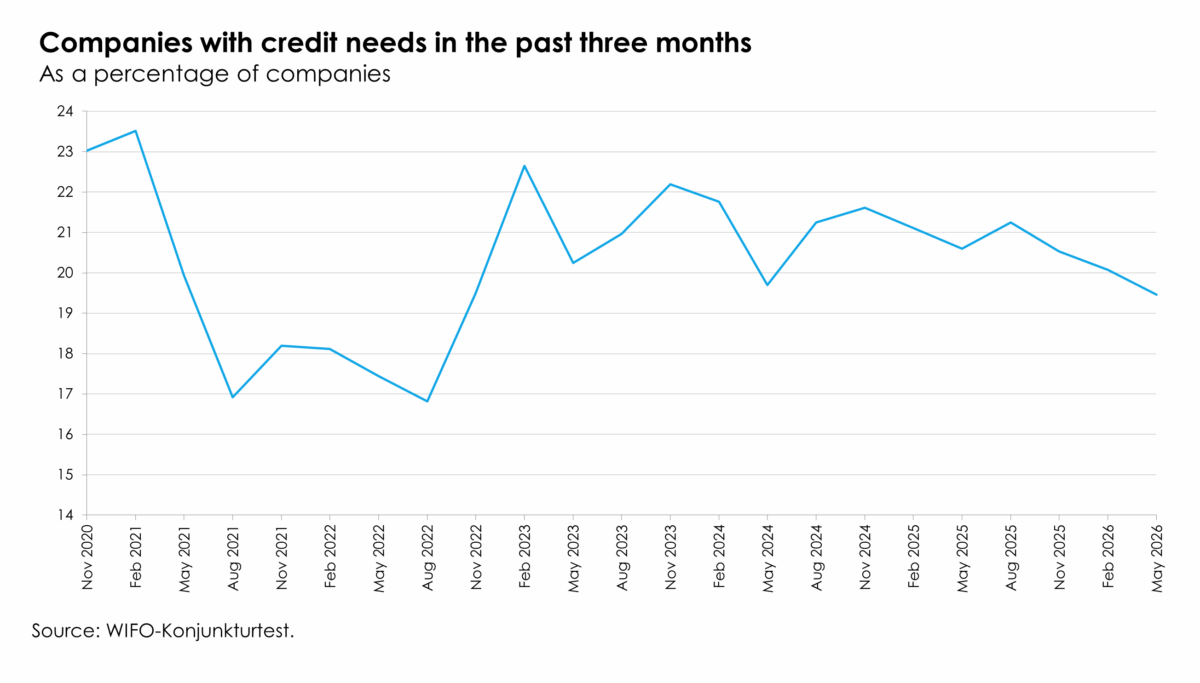

Credit Conditions of Austrian Companies

The credit questions of the WIFO-Konjunkturtest (business cycle survey) allow us to present the assessments and experiences of companies with regard to bank lending. The credit questions are asked quarterly in February, May, August and November.

In May 2026, companies' assessments of banks' willingness to lend – defined as the balance of the proportion of companies that describe banks' lending as accommodative (positive values) and the proportion of companies that describe banks' lending as restrictive (negative values) – improved slightly compared with the previous quarter (+0.8 points) and remained in negative territory at –13.9 points. Differences are evident across company sizes: the credit barrier is higher for smaller companies (fewer than 50 employees) (–16.3 points) than for medium-sized companies (50 to 250 employees: –7.9 points) and large companies (more than 250 employees: –14.4 points).

The survey results show a slight decline in credit demand overall (excluding the retail sector), with a figure of 19.5% (long-term average: 20.8%), representing a decrease of 0.6 percentage points compared with the previous quarter. In the manufacturing sector, demand for credit remained above average (22.1% of companies reported a need for credit), whilst in the retail sector (12.8%) it fell significantly; demand for credit in the service sectors (18.5% of companies) and in the construction industry (19.4%) was average. By company size (excluding retail), 18.9% of smaller companies (fewer than 50 employees) recently reported a need for credit, as did 21.8% of medium-sized companies (50 to 250 employees) and 18.8% of larger companies (more than 250 employees).

Of the companies with credit needs (excluding retail), around 31.5% had to make concessions regarding the amount or the terms (17.5% reported worse terms, 6.7% a lower amount and 7.3% both worse terms and a lower amount than expected). This figure is below the average for the past five years (33.7%). Around 37.8% of companies requiring credit were able to obtain it as expected (5-year average: 37.9%). At 31.7%, the proportion of companies requiring credit that did not receive a loan or had not applied for one was above average (5-year average: 28.4%; around 6.2% of all companies surveyed) because the loan application was rejected by the bank (7.1%), the terms were unacceptable (12.1%) or they had not attempted to secure a loan because they felt it was futile (12.5%).

Credit Constraints and Credit Needs

Recent issues: WIFO-Konjunkturtest

Quarterly results of the WIFO-Konjunkturtests

Special issues: WIFO-Konjunkturtest

Recent issues: WIFO-Investitionsbefragung

Contact

(Senior) Economists

For general enquiries, please contact konjunkturtest@wifo.ac.at.