Overinflation in Austria Contained

"Overinflation in Austria has been contained. However, the cumulative rise in consumer prices in recent years has been much stronger than in the euro area", says Stefan Schiman-Vukan, author of the latest WIFO Business Cycle Report.

Despite numerous interest rate hikes over the past two years, the US economy remained on a growth path in the second quarter of 2024, not least due to the expansionary fiscal policy and cheap legacy credit. In China, the economy lost momentum, prompting the central bank to cut interest rates. Meanwhile, the Bank of Japan unexpectedly raised its key interest rate, triggering stock market turmoil that spread to stock markets elsewhere. In the EU, GDP grew moderately in the second quarter, with the Spanish economy again proving particularly buoyant, while German output contracted slightly.

In Austria, real GDP stagnated in the second quarter compared to both the previous quarter and the previous year. While value added in industry and construction continued to shrink, the service sectors expanded slightly, particularly the public sector. Investment in intellectual property is the only component of demand that is likely to have increased compared to a year earlier, while investment in machinery and equipment and in construction in particular declined.

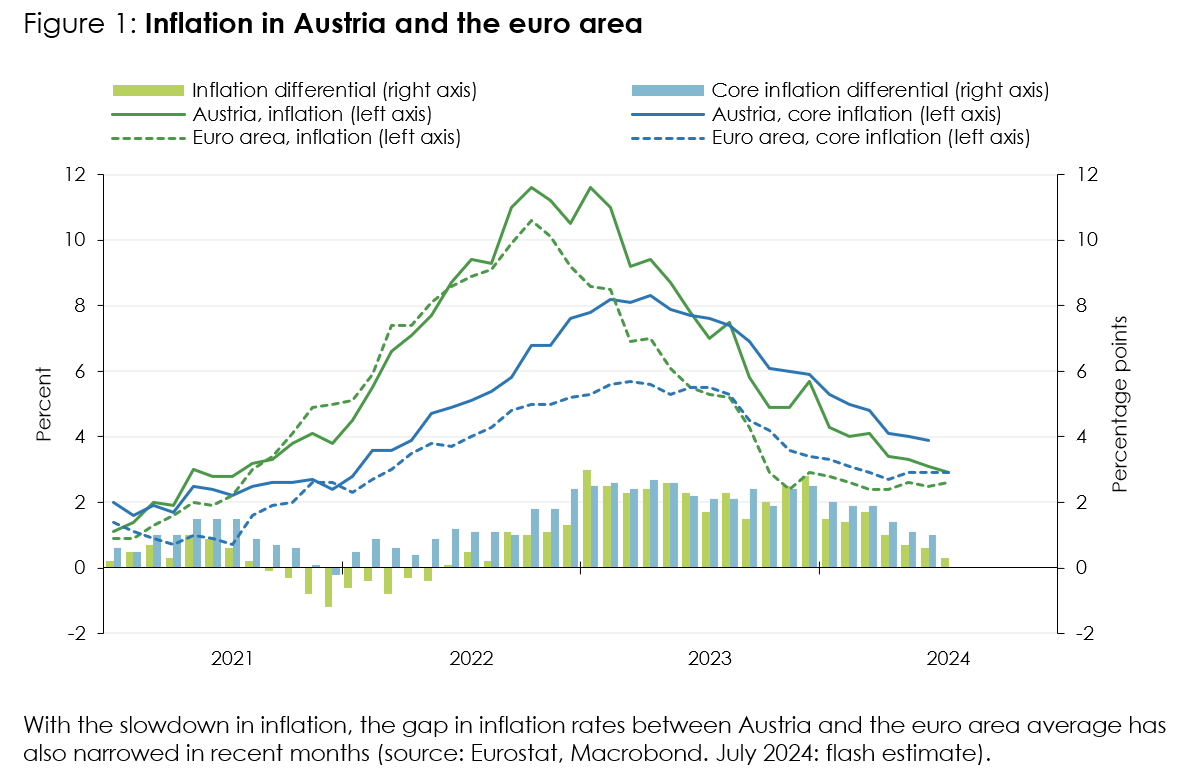

Inflation has normalised relative to the euro area average, with the gap narrowing from 2.8 percentage points in December 2023 to 0.3 percentage points in July 2024. However, the cumulative increase in consumer prices in recent years has been much stronger than in the euro area. The overinflation was driven by buoyant demand for leisure and tourism services, fiscal policy measures and strong wage increases. The wage share has risen sharply since the beginning of 2023, while capital income has fallen steadily.

The sentiment among domestic companies remains extremely pessimistic, particularly in manufacturing. Capacity utilisation in industry has been low for a year now. More and more companies are seeing a deterioration in their competitive position, especially on foreign markets.

Unemployment has continued to rise recently, with the seasonally adjusted unemployment rate standing at 7.1 percent in July, 0.9 percentage points higher than at the previous turning point. Employment continued to increase in the second quarter compared with a year earlier, with almost all new jobs being created in the public sector. Employment growth among women aged 60 and over has accelerated since the statutory retirement age was raised in January 2024. Further supply-side stimuli resulted from the influx of workers from abroad and the integration of refugees into the labour market.

Please contact

Further news