Recession in the Manufacturing Sector Continues – Leading Indicators Improve

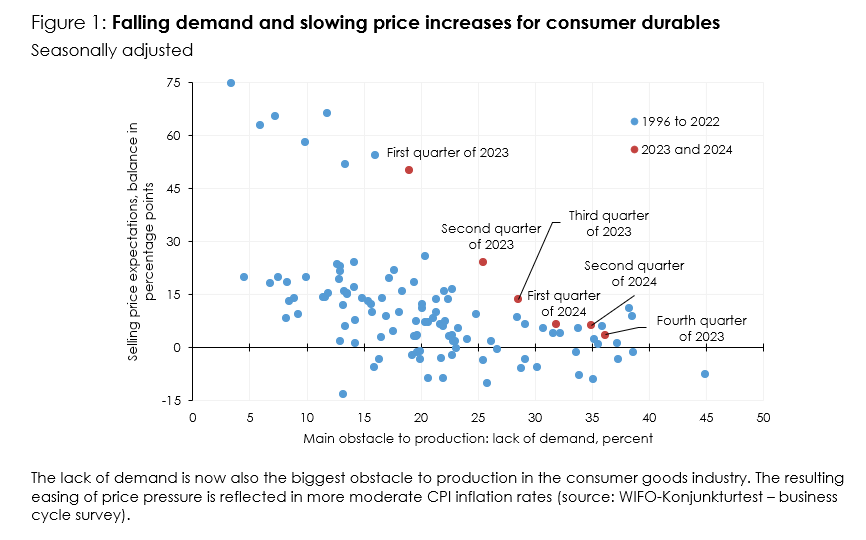

"The weak demand for consumer goods is an obstacle to production on the one hand, but reduces price pressure on the other," says Christian Glocker, author of the latest WIFO Business Cycle Report.

Although the global economy grew somewhat more strongly again in the first quarter of 2024, regional differences remained pronounced. Significant expansion in the emerging markets contrasted with weak growth on average in the industrialised countries. This divergence has now persisted for almost two years.

According to the WIFO Flash Estimate, the Austrian economy is likely to have grown slightly in the first quarter of 2024 (+0.2 percent), after GDP had stagnated in the previous quarter. In industry (NACE 2008, sections B to E) and construction, value added fell once again, meaning that the recession in these sectors continued at the start of the year. Only consumer-related market services expanded and thus supported the total economy. On the demand side, private consumption increased, while investments continued to shrink sharply. Exports also declined. As a result of the sharp decline in imports, foreign trade made a positive contribution to gross domestic product in purely arithmetical terms. Nevertheless, the decline in imports reflects the persistently weak demand for domestically produced goods.

Leading indicators remain at a low level, although they have recently improved somewhat. According to the WIFO-Konjunkturtest (business cycle survey), assessments by construction and industrial companies remain pessimistic, while market service providers are largely more confident. Consumer confidence remains very low.

Inflation has weakened further recently, but remains high compared to many other euro countries. The decline in producer prices that has been observed for some time, which in turn is due to the fall in energy prices, is now significantly dampening consumer price inflation (March: 4.1 percent compared to the same month last year, flash estimate for April 3.5 percent; according to CPI).

The economic weakness is reflected in the labour market. In industry, construction and some service sectors, employment shrank significantly in the first quarter of 2024 compared to the previous quarter (according to the quarterly national accounts). Only in public-related service sectors did it increase strongly once again. Unemployment continued to rise recently, while the number of job vacancies fell. According to preliminary estimates, dependent employment in April 2024 was 6,000 jobs higher than in the previous year (+0.2 percent). At the end of April, around 29,000 more people were registered as unemployed than a year ago (+11.2 percent), while there were also around 8,000 more persons in AMS training (+10.7 percent). The unemployment rate (national definition) is therefore likely to have been 6.8 percent (+0.6 percentage points above the previous year).

Please contact