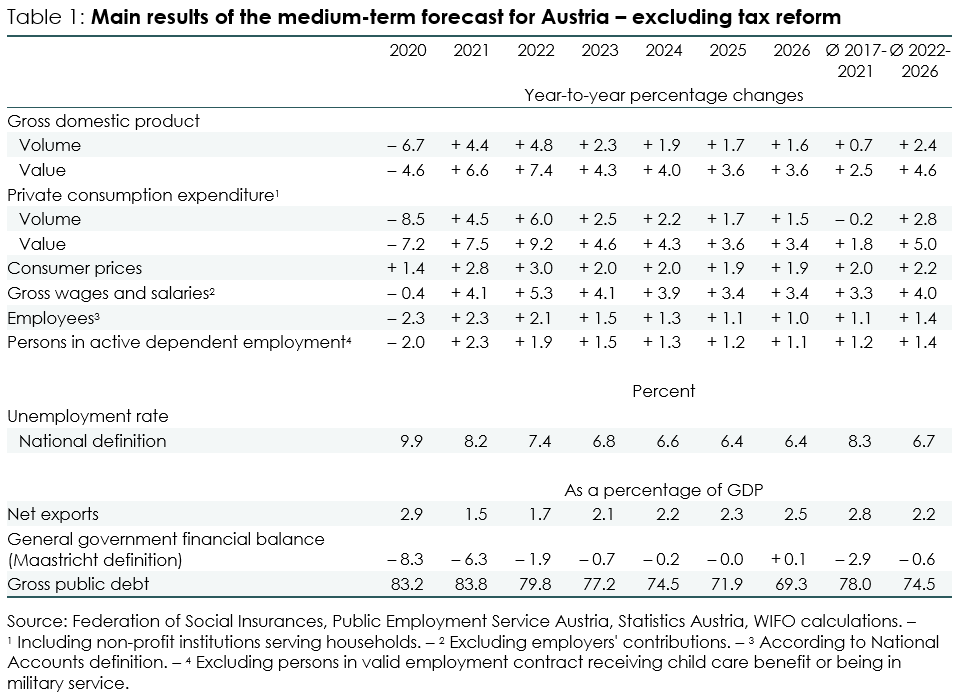

Medium-term Forecast for 2022 to 2026

The very rapid and strong recovery of the global economy and a strong rebound effect in domestic private consumption, services exports and private investment lead to strong growth in 2021 (+4.4 percent) and 2022 (+4.8 percent)1. In the years 2023 to 2026, growth is expected to remain above average (+1.9 percent p.a.) compared with the pre-crisis period (Ø 2010-2019 +1.5 percent p.a.; Table 1). Due to the assumed frontloading effects from the investment premium in 2021-22, a weaker dynamic in private fixed capital formation is assumed as an echo effect for the years 2023 and 2024.

Private consumption is perceived as the main driving force behind the domestic recovery. Household incomes were stabilised in 2020 and 2021 by fiscal policy measures (especially short-time work). As COVID-19 regulations significantly restricted consumption options during this period, private savings (primarily through "forced savings") were significantly expanded: the savings rate rose from 8.5 percent (2019) to 14.4 percent (2020) and 10.4 percent (2021). With the end of across-the-board restrictions, private consumption spending is expected to expand significantly from the second half of 2021 onward. For 2022, a savings rate already below the pre-crisis level is assumed (6.0 percent). Consumption growth in subsequent years (Ø 2023-2026 +2.0 percent p.a.) is also expected to be stronger than in the pre-crisis years (Ø 2010-2019 +0.9 percent p.a.). By the end of the forecast period, the savings rate could therefore fall to 4.5 percent.

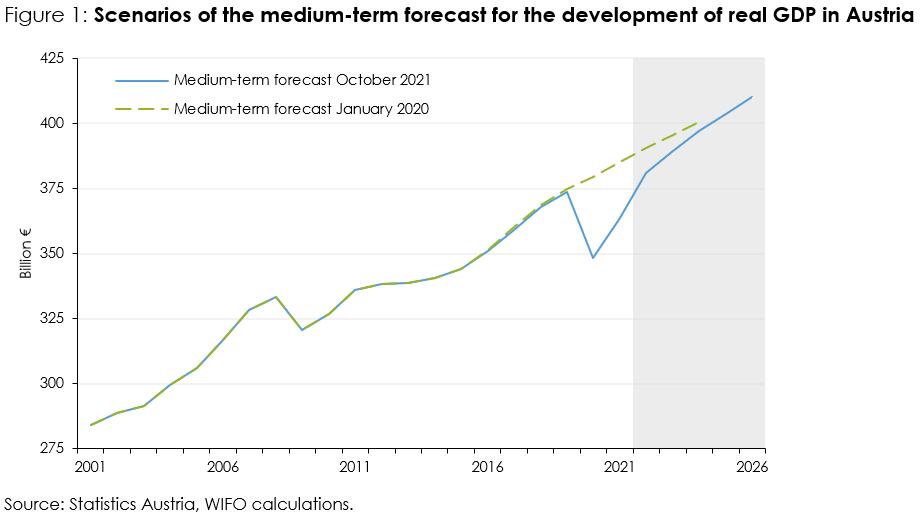

Due to the strong recovery, a return to the growth path prior to the COVID-19 recession is assumed by the end of the forecast horizon: compared with a scenario without COVID-19 recession – the WIFO medium-term forecast to 2024 of January 2020, which was not yet affected by the COVID-19 pandemic2 – the gap in the real GDP level in 2024 is now estimated at 0.9 percent (Figure 1). The pre-crisis GDP level is expected to be reached in the third quarter of 20213.

In comparison with the recovery after the global financial market and economic crisis in 2008-09, the recession-induced GDP gap is expected to close more quickly after the COVID-19 crisis.

The labour market will also benefit from the stronger recovery. The unemployment rate is expected (on an annual average) to reach pre-crisis levels in 2022, and by the end of the forecast horizon the number of unemployed persons is estimated at 276,000 (2020: 410,000).

The rise in the rate of inflation to 3.0 percent in 2022 is primarily driven by energy (mineral oil products, natural gas and electricity) and industrial goods (e.g. furniture, clothing, household appliances, consumer electronics). These areas are affected by substantial price increases for raw materials and intermediate products, sharp rises in transport costs, and supply shortages and delivery delays. This situation is expected to ease in the second half of 2022, driven not at least by supply expansions triggered by soaring prices. In the case of services, in 2022 the withdrawal of the VAT cut in the sectors mostly affected by the pandemic (or the measures adopted to contain it) is likely to be partially transmitted to prices. However, all these developments are mainly temporary price increases that do not trigger a sustained upward inflation trend. Real wage growth is expected to be lower than labour productivity growth over the forecast period, suggesting that domestic labour costs should not contribute excessively to inflation and not set off a wage-price spiral. Average annual price inflation of 2 percent is expected from 2023 to 2026.

Most of the support measures adopted in the course of the COVID-19 crisis were enacted as temporary measures and will therefore only lead to a transitory increase in government spending. As the economy recovers, revenues should rise again significantly. As the crisis abates, the build-up of public debt will therefore slow down significantly from 2022 onward. Under the "no-policy-change" assumption4 underlying the WIFO forecasts, the government budget deficit for 2021 is still 6.3 percent (fiscal balance as a percentage of nominal GDP), which is expected to fall to 1.9 percent in 2022. Under these assumptions, a balanced budget (+0.1 percent) is expected for 2026. The government debt ratio (as a percentage of nominal GDP) is expected to decline from its peak of 83.8 percent in 2021 to 69.3 percent by the end of the forecast horizon. This decline in the debt ratio is mainly due to the significant increase in nominal GDP (Ø 2022-2026 +4.6 percent p.a.).

1 Schiman, S. (2021). Prognose für 2021 und 2022: Vierte COVID‑19-Welle bremst kräftigen Aufschwung. WIFO. https://www.wifo.ac.at/wwa/pubid/67991.

2 Baumgartner, J., & Kaniovski, S. (2020). Update der mittelfristigen Prognose der österreichischen Wirtschaft 2020 bis 2024. WIFO-Monatsberichte, 93(1), 33-40. https://monatsberichte.wifo.ac.at/62440.

3 Baumgartner, J. (2021). Weekly WIFO Economic Index. WWWI: Calendar Week 36 and 37 2021. WIFO. https://www.wifo.ac.at/en/news/weekly_wifo_economic_index (retrieved on 6 October 2021).

4 In general, the WIFO forecasts only consider laws and regulations that have already been passed. In certain cases, measures that have not yet been formally adopted are also included. This is the case, for instance, when the negotiation or law-making process is already well advanced (draft laws under review; in some cases, Council of Ministers decisions are also included) and sufficiently detailed information is available on the regulation in question to allow a quantitative assessment.

Please contact