Global Factors Account for Half of Inflation

Inflation continues to be driven to a large extent by commodity prices, which have recently risen strongly due to the price of natural gas. Half of inflation is caused by global demand impulses (upswing of the world economy) and global supply shocks (supply and delivery bottlenecks). In the USA, the recovery is already further advanced than in the euro area, and monetary policy there is increasingly being tightened. Austria recorded one of the sharpest GDP declines in the euro area in the fourth quarter of 2021 – as it did in the final quarter of 2020. However, the domestic labour market weathered the fourth lockdown largely unscathed. Particularly in the manufacturing sector, optimism prevails despite material shortages and recruitment difficulties.

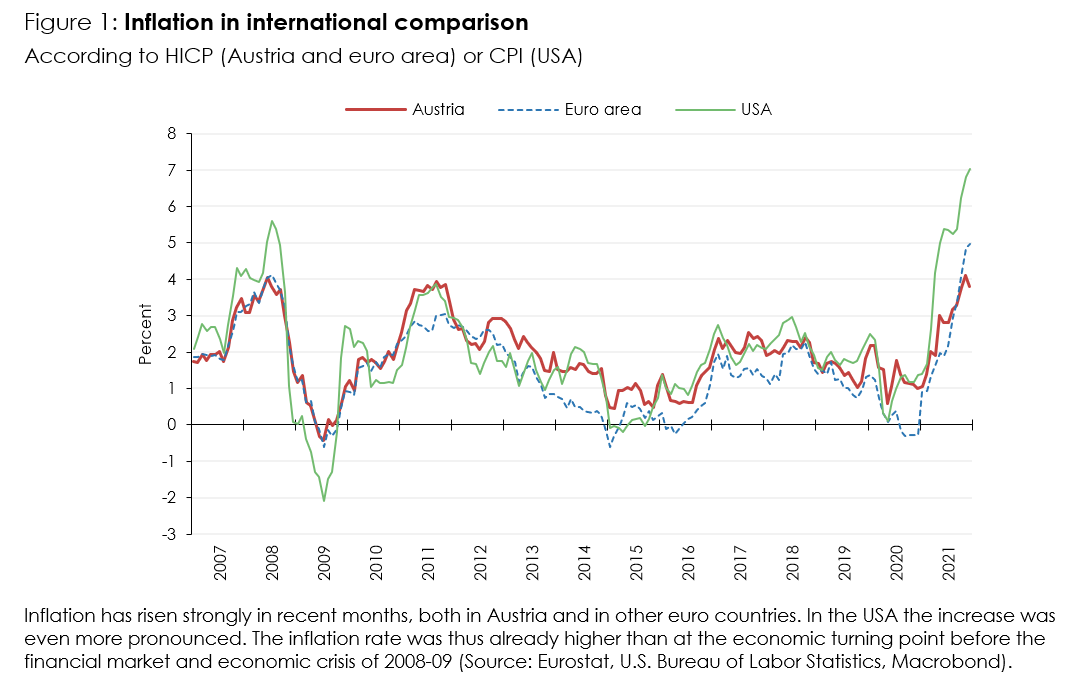

According to the flash estimate, HICP inflation rose to 5.1 percent in the euro area and to 4.6 percent in Austria (or 5.1 percent according to CPI) in January 2022. A large part of the increase is due to the rise in commodity prices. Most recently, the drastic increase in the price of natural gas fuelled inflation. Accordingly, about half of the inflation rate is due to global factors: 30 percent is due to supply bottlenecks, 20 percent to positive demand impulses from the upswing in the world economy.

Tightening monetary policy is more clearly warranted in the case of demand-side inflation than in the case of supply-side inflation, as the latter also has negative real economic effects. While in the USA the share of demand-driven inflation in overall inflation had been high for a while now, that level was reached only recently in the euro area. Therefore, the Federal Reserve is initiating the interest rate turnaround earlier than the ECB. It will end its bond purchases and raise the key interest rate as early as March. Further interest rate hikes and bond sales will follow later in 2022.

After a strong growth spurt in the fourth quarter of 2021, value added in the USA is already a good 3 percent above the pre-crisis level. In the euro area, after a weak end to 2021, it is only at a similar level as in the fourth quarter of 2019 before the outbreak of the COVID-19 pandemic. Austria was among the euro area countries with the sharpest GDP decline in the fourth quarter of 2021, as it was in the final quarter of 2020. Economic output also declined in Germany. In addition to more severe lockdowns as a result of low vaccination rates, this was also due to greater exposure to supply problems in both countries.

Despite material bottlenecks and recruitment difficulties, optimism in industry and the construction sector in Austria is unbroken. Sentiment in the service sector is more ambivalent. Although confidence prevails in some sectors here as well, accommodation and food services are clearly pessimistic in their assessments.

The domestic labour market has weathered the fourth lockdown largely unscathed, not least because of the use of short-time work, but also because many foreign seasonal workers did not come to Austria at all. This decline in labour supply is increasingly worrying companies. Already now, the labour shortage is affecting business activity in many sectors. In spring 2021, the labour supply had still recovered quickly after the lockdowns.

Publications

Please contact

Further news