Family bonus: limited macroeconomic effects

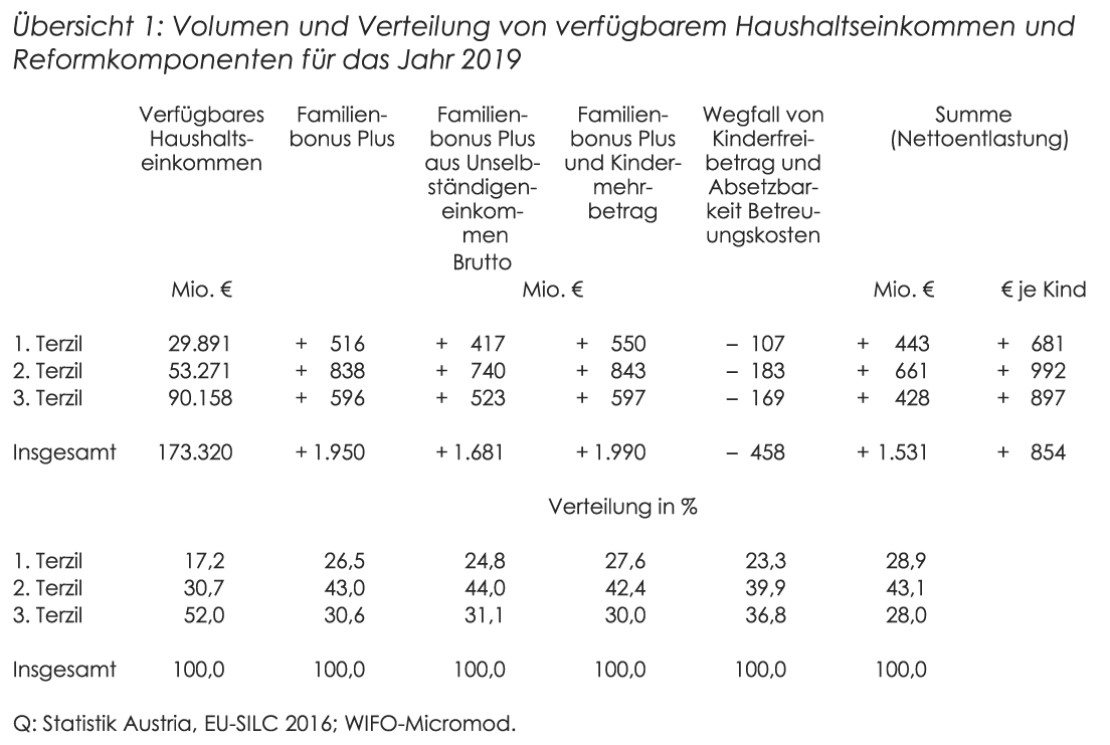

At the centre of this work is an estimate of the medium-term macroeconomic effects of the family bonus plus and the additional child benefit, which will replace the child allowance and the tax deductibility of childcare costs from 2019. According to WIFO estimations, the introduction of the family bonus plus and the additional child allowance, taking into account the abolition of the child allowance and the tax deductibility of childcare costs, will reduce the tax burden primarily for middle-income households (Table 1).

According to WIFO estimates, 43 percent of the total net relief is attributable to households in the middle third of the income bracket, where the average annual net relief per child amounts to 992 euro. In the lower third of the income bracket, the family bonus cannot be fully utilised as incomes are too low. This group accounts for 29 percent of total relief and the annual average net relief per child is 681 euro.

In the upper third of the income bracket, the higher average age of the children – for children over 18, the family bonus amounts to a maximum of 500 euro per year – and the comparatively higher loss due to the abolition of the allowances have a significant effect. This group accounts for 28 percent of the total relief and the annual average net relief reaches 897 euro per child.

This estimation was based on the assumption that the family bonus would be fully utilised and optimally distributed between the parents.

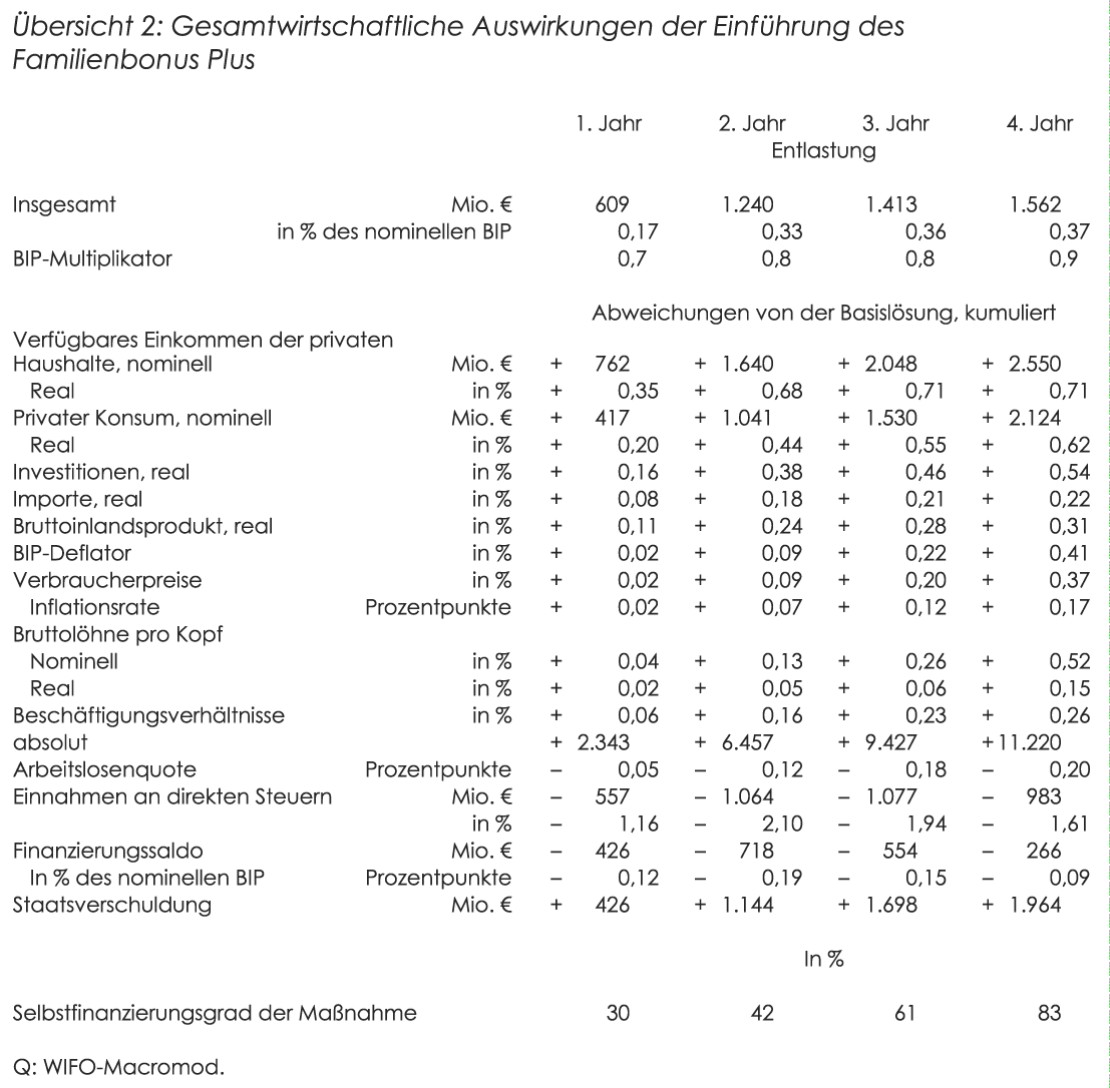

The tax loss already incurred in 2019 as a result of the use of the family bonus by employed parents via the company payroll accounting is assumed to be 609 million euro. From 2020, the family bonus will be fully effective, as households that claim the family bonus and the additional child allowance via the income tax assessment will also benefit from the tax relief.

The net relief will rise from 1.24 billion euro in 2020 to 1.56 billion euro in 2022. The WIFO estimates take into account both the increase in net relief due to annual increases in income and the entitlements for children living abroad, taking into account the different cost of living in Austria and in the countries of residence.

The relief from wage and income tax increases the disposable incomes of households, which in turn increases private consumption and economic performance. As a result of the acceleration in growth, employment is increasing and unemployment is falling. The increase in demand also causes an increase in the price level.

The simulations with the WIFO Macromod show that after four years (2022) real GDP will have increased by 0.3 percent cumulatively compared to the basic solution without tax relief, the number of employment relationships by 11,000 (+0.3 percent) and real wages per capita by +0.15 percent (Figure 2). The increase in demand will be accompanied by an annual rise in the inflation rate of 0.1 percentage point.

Additional demand impulses triggered by the wage and income tax relief lead to additional revenues from direct and indirect taxes and social security contributions. This halves the deterioration in the government fiscal balance compared to the second year. This will result in an increase in government debt of 1.96 billion euro by 2022.

In these estimations, no other counter-financing measures were implemented apart from the abolition of the child allowance and the deductibility of childcare costs. Depending on their design, the macroeconomic effects described would thus be lower.

Publications

Please contact