Domestic Economy in Good Shape Before Outbreak of War in Ukraine

Economic output in Austria was again above the pre-crisis level in February. The prospects in the sectors most affected by the fourth lockdown have recently brightened considerably, especially in accommodation and food services. The domestic unemployment rate, seasonally adjusted, is at its lowest level since the outbreak of the financial market and economic crisis in 2008, and the number of job vacancies has reached a new high. Inflation recently rose to just under 6 percent and is likely to remain high for longer due to commodity price shocks related to the Ukraine war. A possible disruption of Russian natural gas supplies poses risks for certain sectors of domestic industry.

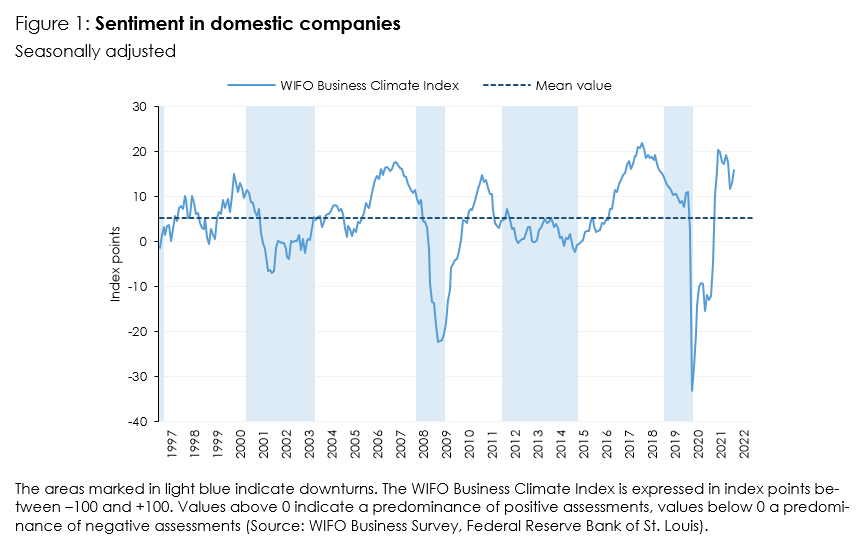

The Austrian economy has quickly overcome the effects of the fourth lockdown. GDP had already returned to pre-crisis levels by the end of 2021 and only temporarily weakened somewhat at the beginning of 2022 due to the omicron wave. Although value added in industry is currently stagnating due to the expensive intermediate products, the optimism of companies is unbroken in view of the good order situation. In the services sector, the outlook has brightened especially in tourism. Although the current situation in tourism is still considered unfavourable by the majority, the nascent recovery from the COVID-19 pandemic and the positive booking situation are making businesses increasingly confident.

The domestic labour market is already in a boom. Employment and the number of job vacancies have reached new highs and the seasonally adjusted unemployment rate in February was at its lowest level since the outbreak of the financial market and economic crisis in 2008. The crisis-related rise in long-term unemployment has also already been reduced by 84 percent.

The war in Ukraine will somewhat slow down the upswing in the euro area and in Austria. The already very high commodity prices received a new boost as a result, which will dampen the real incomes of private households for a protracted period of time. If the supply volumes of Russian natural gas are curtailed, there would be production losses in some areas of industry over the year. Among domestic banks, only Raiffeisen Bank International has a substantial exposure to Russia. However, domestic lending is not likely to be significantly affected by Russia's ousting from the international financial system, as in the Raiffeisen Group this is handled via regional banks and Landesbanken. Direct foreign trade in goods with Russia has declined since the Crimea crisis and the related sanctions. The volume of trade is now low.

For central banks, the recent commodity price shocks pose a major challenge. Already so far, the strong rise in inflation has been largely driven by unfavourable supply shocks, which makes tightening monetary policy difficult. The war in Ukraine has increased the dilemma for central banks, especially the ECB. Despite the further acceleration of inflation – in Austria to presumably almost 6 percent in February – the central banks could again deviate somewhat from the tightening course they have recently adopted.

Publications

Please contact