Austria's Economy Remains in Crisis

"The current recession in manufacturing is the second-longest crisis in over 20 years. So far, only the crisis at the beginning of the 2000s has lasted longer, but the production losses back then were significantly lower," says Marcus Scheiblecker, author of the latest WIFO Business Cycle Report.

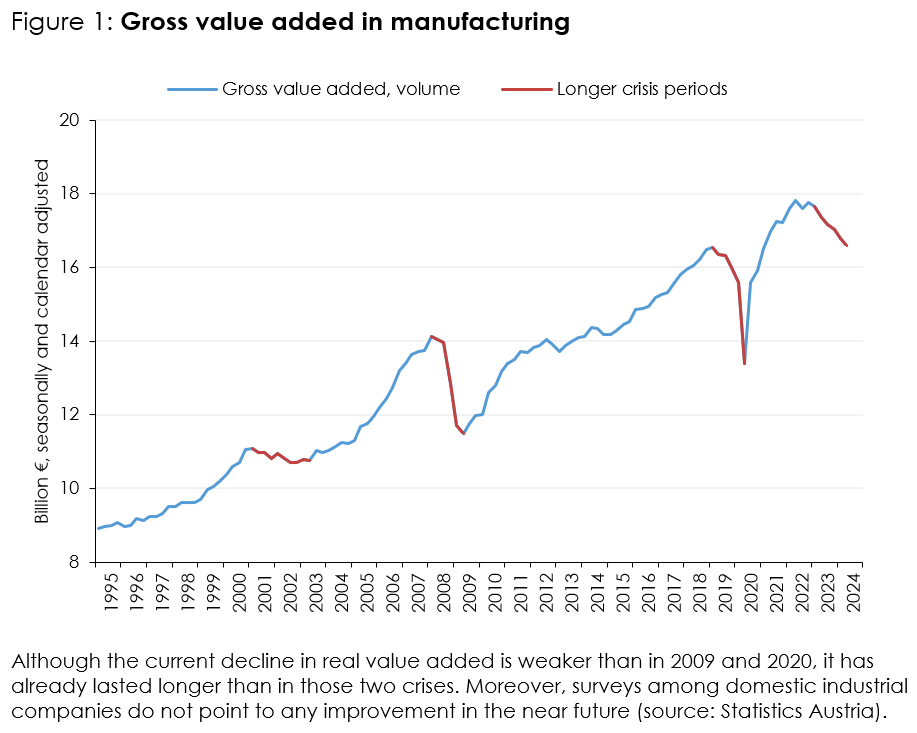

Domestic manufacturing is still mired in recession. The declines in the last six quarters mark the third sharpest drop in production after the 2008-09 financial market and economic crisis and the COVID-19 crisis. Despite the length of the downturn, company surveys do not yet indicate an improvement.

Like the industry, Austria's construction sector is suffering from a pronounced lack of demand. Over the past nine quarters, residential construction investment fell by around 18 percent in volume terms. Although non-residential construction contracted at a much lower rate over the same period (around –6 percent), it has been declining since the second half of 2020. In the first quarter of 2024, non-residential construction investment reached its lowest price-adjusted level since 1995.

Leading indicators for Austria and the euro area suggest that economic momentum will remain subdued in the coming months. The lack of demand for industrial goods is having a particularly negative impact on euro area countries that specialise in this sector, such as Germany and Austria. Economies with a more important services sector, like France and Spain, have recently achieved at least slight growth. In almost all euro area countries, the construction sector – especially the building construction – is holding back GDP growth.

In the USA, the favourable business cycle should continue, given the positive sentiment among companies and private households. Only expectations for industrial production have deteriorated.

In addition to weak international demand, the Austrian economy is suffering from hesitant consumer demand, as well. Although last year's high wage settlements continue to have a positive effect on incomes and inflation has fallen significantly since the beginning of the year, private households are very reluctant to spend. According to Statistics Austria, nominal retail sales (excluding the motor vehicle trade) rose by just 0.4 percent year-on-year in the second quarter of 2024. In volume terms, this corresponds to a decline of 1.6 percent.

Inflation continued to fall in August to 2.4 percent (flash estimate; July 2.9 percent). Especially lower prices for petroleum products had a dampening effect.

The domestic labour market is increasingly suffering from the economic downturn. Dependent employment has barely grown in recent months, while the number of vacancies registered with the Public Employment Service (AMS) has fallen significantly compared to the previous year. The unemployment rate is trending upwards.

Please contact