Austria is Growing More Slowly than the Average of the Euro Countries

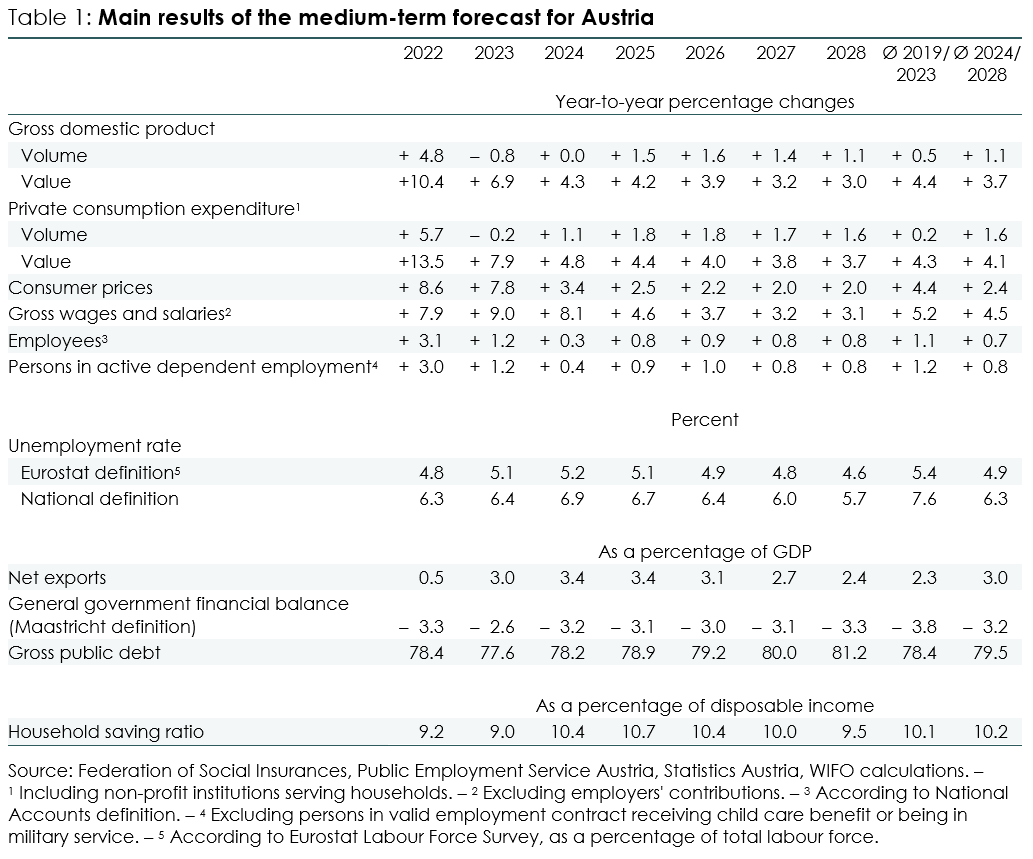

In the most important countries and country groups for the Austrian export industry (euro area, CEEC 5, USA, China, Switzerland), economic growth (export-weighted) is expected to increase from ¾ percent (2023) to 2 percent (2025) and then slow down again slightly (2028 +1½ percent).

Following the interest rate cut in June (–¼ percentage point), WIFO anticipates that the ECB will implement another interest rate cut for the euro area in autumn. Over the medium term, the three-month interest rate is expected to decline from 3.7 percent (2024) to 2½ percent (2028). The secondary market yield on 10-year German government bonds is likely to decrease from 2¾ to 2 percent. Based on the described growth and interest rate trends in the USA and the euro area, the exchange rate of the dollar against the euro will remain almost constant (1.09 $ per € in 2024, 1.06 $ per € in 2028).

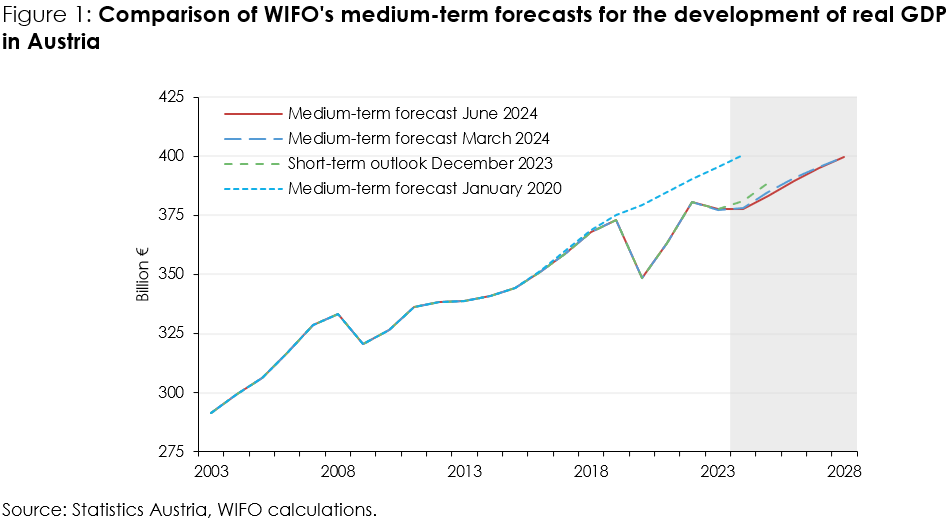

Over the forecast horizon, Austria is likely to experience slightly weaker growth than the average for the euro countries. WIFO's assessment indicates that this is primarily due to a deterioration in international competitiveness as a result of higher wage increases and higher energy prices in Austria.

Over the forecast period, private real consumption is expected to be the main growth driver, with an annual growth rate of +1½ percent. This development will be accompanied by a decline in the savings rate (2025: 10.7 percent, 2028: 9.5 percent), although the level of the savings rate is expected to be above the long-term average from before the COVID-19 and inflation crisis (Ø 2010-2019: 7.8 percent).

The global economy is expected to recover, which will stimulate exports. In 2024-2028, exports are projected to grow by 2 percent annually in volume terms. Import growth will depend on the domestic economy and exports. In 2024-2028, import growth is expected to be 2¼ percent p.a. This will result in a fall in the surplus in net exports from just under 3½ percent (2024) to 2½ percent of nominal GDP (2028).

Investment in equipment and machinery (including other fixed capital formation) is likely to shrink by nearly 1 percent in 2024. In 2025, growth is expected to reach 3 percent due to the international economic recovery, the decline in interest rates and the corporate tax rate, and the favourable impact of the (eco) investment allowance. While the switch to lower-carbon emission production methods requires increased investment in the energy transition, manufacturers in particular may be reluctant to invest due to the challenging geopolitical environment and rising unit labour costs. Growth is expected to average 2 percent per year in 2026-2028.

The slowdown in construction activity will continue in 2024, with a decline of 4¼ percent in construction investment. This primarily affects residential construction, due to high inflation, which has resulted in a reduction in real disposable household income. Furthermore, tighter lending rules, including the KIM regulation, which is still in force until mid-2025, and higher lending rates will make it significantly more difficult to finance housing over the entire forecast horizon. Both of these factors will dampen demand for residential construction. From 2025, WIFO anticipates a recovery in construction investment (2026-2028 +1½ percent p.a.) due to the general economic recovery and catch-up effects. The housing initiative adopted by the federal government should also have a stimulating effect in 2025-2026.

The economic stagnation will merely enable a weak increase in employment of 0.4 percent in 2024. As the economy recovers, employment growth is likely to increase to just 1 percent by 2026 and is expected to weaken slightly towards the end of the forecast period due to the economic cycle. Demographic change will intensify the labour shortage over the forecast period – the labour supply is likely to rise by 0.6 percent per year. Furthermore, we anticipate an increase in the labour force participation of women and older people (due to the gradual increase in the standard retirement age for women from 2024 and a higher qualification level among the elderly), as well as a sustained increase in the supply of labour from non-Austrian citizens. The weaker labour supply in the medium term also dampens the trend growth prospects but reduces unemployment. The unemployment rate is expected to fall to 5.7 percent by 2028 (6.9 percent in 2024).

Inflation (according to the CPI) remained exceptionally high in 2023 (7.8 percent) after 8.6 percent in 2022. However, the focus of inflation shifted from energy prices to the areas covered by core inflation. This trend will continue in 2024, with labour-intensive services being the main driver of price increases. After 3.4 percent in 2024, inflation will slow to 2 percent by mid-2026 and thus reach the ECB's medium-term target.

In Austria, wage negotiations are based on the average inflation rate of the previous 12 months (rolling inflation). As a result, gross real wages per capita will continue to rise, albeit at a decreasing rate, over the coming years. A real wage increase of 4.2 percent is forecast for 2024, which will largely offset the real wage loss in 2022. WIFO anticipates a deceleration in real wage growth between 2025 and 2028, as the discrepancy between rolling inflation (the basis for wage demands) and anticipated inflation in the subsequent year narrows.

Compared to the period 2010-2019, the period after the financial market and economic crisis and before the COVID-19 crisis, average annual real wage growth will nevertheless be 1 percentage point higher in 2024-2028. Consequently, unit labour costs will also increase significantly, albeit at a decreasing rate (2024 +8¼ percent, 2025 +3 percent, 2028 +2 percent, average 2010-2019 +1.7 percent p.a.). Real wages (per capita, 2024-2028 +1¼ percent p.a.) are therefore likely to experience stronger growth than productivity (+½ percent p.a.) in the forecast period.

The decline in inflation will result in the expiration of temporary support measures designed to cushion the loss of purchasing power and rising energy prices for private households and companies. This will ease the burden on public finances. However, the revenue-side effects of the inflation shock will also be eliminated, particularly in the case of wage-related revenues, income tax and VAT. Furthermore, the compensation of tax bracket effects, which in the past has led to a kind of automatic consolidation of public finances on the revenue side, also has a dampening effect on government revenue dynamics. Meanwhile, the burden of high inflation-related increases in expenditure on public sector wages and salaries, pensions, inflation-adjusted social benefits and service of interest payments will continue over the forecast horizon. Furthermore, the federal provinces and municipalities have obligations under the new financial equalisation scheme to achieve agreed targets in the areas of the environment, housing and primary education and to meet the growing challenges in the health and long-term care sector.

Given this combination of challenges, WIFO anticipates a budget deficit of 3 percent of GDP (or more) each year over the entire medium-term forecast horizon. The government deficits will also result in an increase in public debt, with a gross debt level of around 466 billion € at the end of the forecast period. The government debt ratio is expected to increase from 78 percent of GDP in 2024 to 81 percent in 2028, which is significantly higher than the targets of the revised European fiscal framework.

Please contact

Further news