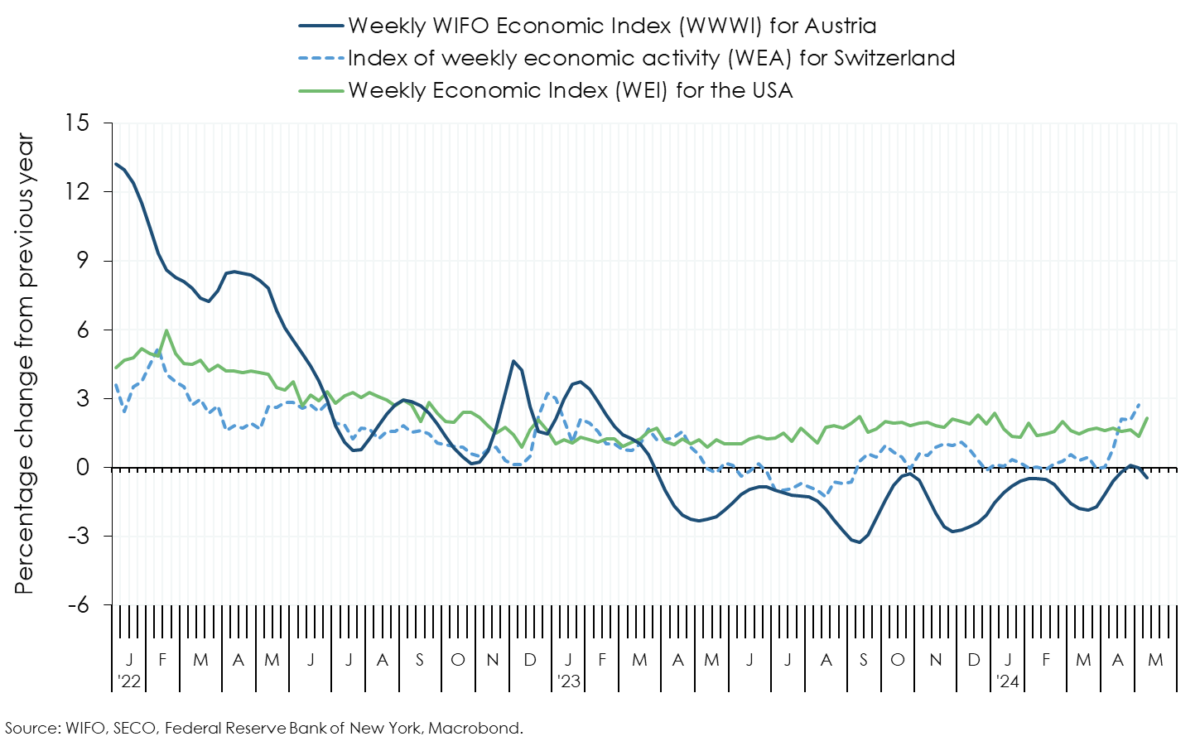

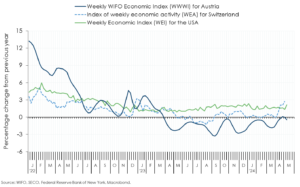

Weekly WIFO Economic Index

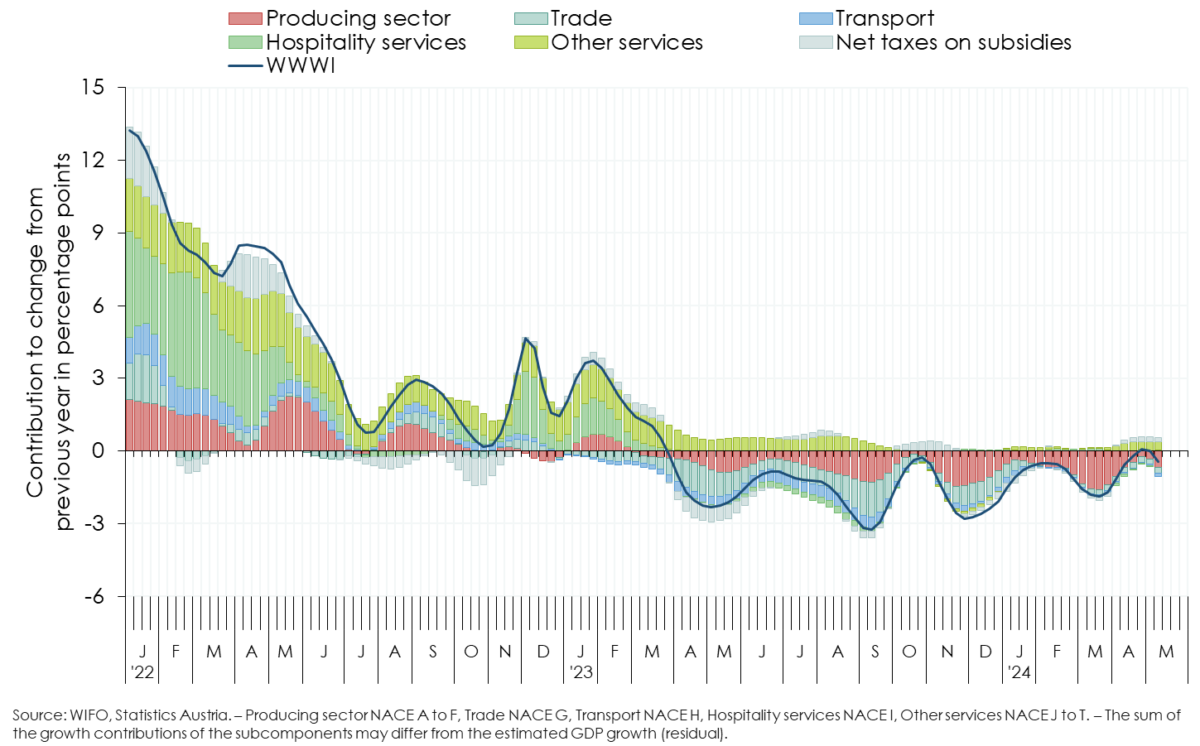

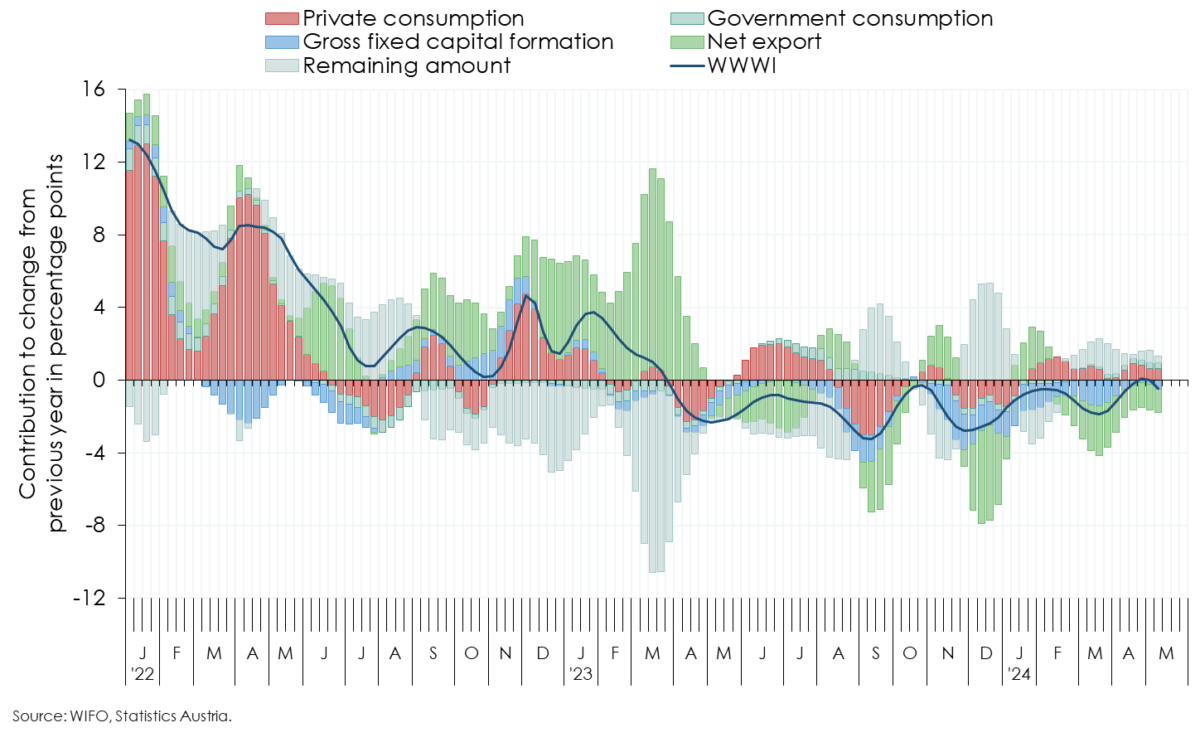

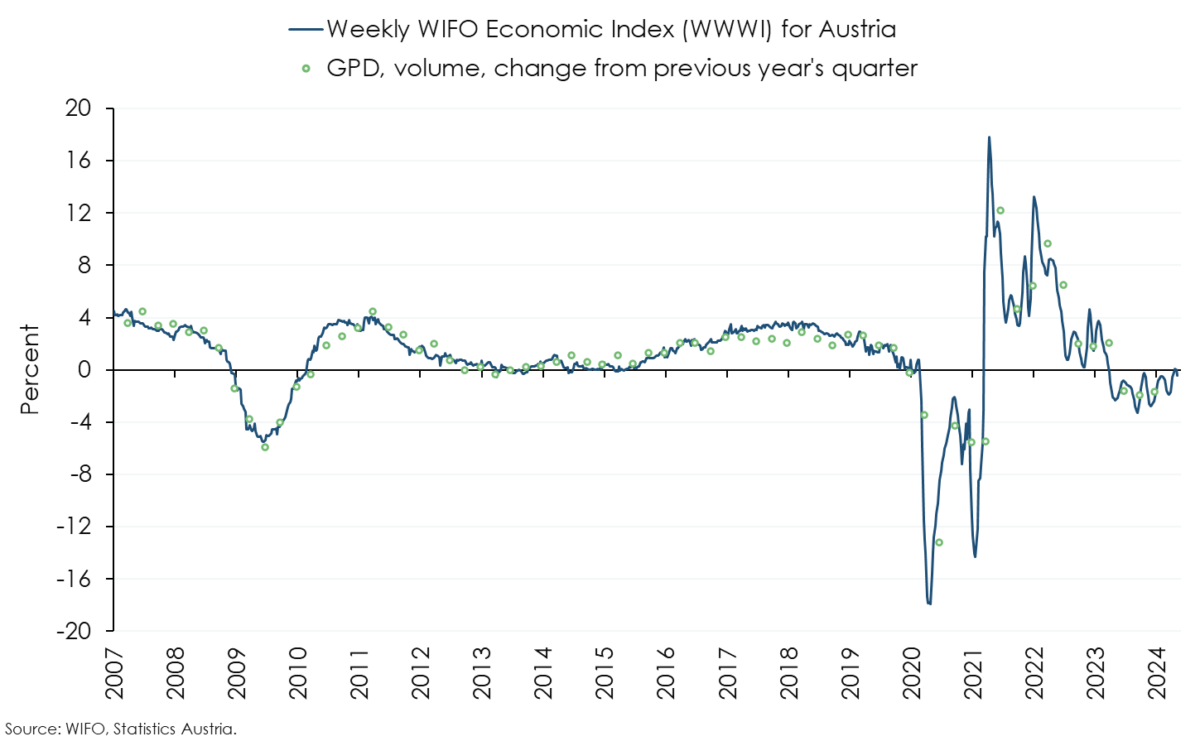

WWWI for GDP and its subcomponents

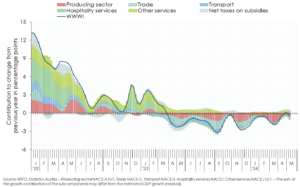

Based on the weekly indicator of real GDP (WWWI), domestic output in April (calendar weeks 14 to 17, 1 to 28 April) was ½ percent and in the first half of May (calendar weeks 18 and 19, 29 April to 12 May) ¼ percent lower than in the same period of the previous year (March –1¾ percent, revised)1. The current calculations for the months February to April are influenced by working day effects, which cannot be corrected by using the year-on-year changes in the model estimates2. In February, an additional working day (leap day on 29 February) affects activity. In 2024, Holy Week and Easter fell in the last week of March (calendar week 13) – in 2023 Easter fell in the first week of April (calendar week 14) – which gave a positive boost to tourism and trade on the output side and to retail trade and private consumption on the demand side in March. For calendar week 14 2024, this in turn led to weaker economic output compared to the same week of the previous year. In 2024, there were 2.5 working days less in March and 2.5 working days more in April than in the previous year. This was mainly reflected in sharp falls in the industrial and construction production indices in March and led to an improvement in the producing sector in April.

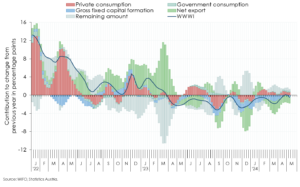

The inflation-adjusted volume of non-cash transactions, as an indicator of household consumption, shows a slight year-on-year decline in demand for goods (retail sales) in April and the first half of May. Demand for services is likely to have been somewhat stronger. Private consumption in April and the first half of May is estimated to have been 1¼ percent higher than a year earlier.

The development of gross fixed capital formation is determined by economic output (industrial production) and sentiment in the manufacturing sector (according to the WIFO-Konjunkturtest, business cycle survey). In April, the decline is estimated at 2 percent year-on-year (March –5½ percent).

Compared to the same period of the previous year, rail freight volumes fell again in April. In contrast, road freight transport on Austrian motorways and the number of flights handled at Vienna airport increased. Overall, exports fell slightly more than imports, leading to a further decline in net exports. The estimated growth contribution of net exports in the broad sense to GDP was therefore negative in April, at –1½ percentage points (March –2½ percentage points).

The development of freight transport is also reflected in the value added of the transport sector (NACE 2008, section H). At –1 percent in April, it remained below the level of a year ago (March –1¾ percent).

The industrial production index slumped by 11.4 percent (unadjusted) in March, not least because there were 2.5 fewer working days than in the previous year. In April, with 2.5 more working days than a year earlier, the picture for industrial production improved. Employment in the goods-producing sector (NACE 2008, sections A to E) continued to fall in April due to the recession, and the number of jobseekers has been rising at double-digit rates year-on-year since November 2023. The WIFO-Konjunkturtest (business cycle survey) does not yet show a sustained improvement in sentiment. WIFO expects value added in the goods producing sector to have been 2 percent lower in April and 1¾ percent lower in the first half of May than a year earlier (March –5½ percent).

Sentiment in the construction sector has stabilised somewhat. According to the WIFO-Konjunkturtest (business cycle survey), both the assessment of the current situation and expectations have improved compared to March, although they remain in negative territory. The rise in the number of persons registered as unemployed in the construction sector, which has been going on for almost 1½ years, has been back in double digits at over 20 percent since March, while employment has been falling for nine months. Value added in construction (NACE 2008, section F) is expected to have fallen by 2¼ percent in April and by 1¾ percent in the first half of May compared to a year earlier (March –4 percent).

Easter effects can also be seen in tourism in March and April. Based on cashless transactions in hotels and restaurants, sentiment indicators from the WIFO-Konjunkturtest and online searches by foreign guests, value added in tourism (accommodation and food services, NACE 2008, section I) is estimated to have been 2 percent lower in April and ¾ percent higher in early May than in the same period of the previous year (March +1¾ percent). In the distributive trades (NACE 2008, section G), was 2 percent lower in April and 2¼ percent lower at the beginning of May than in the previous year (March –2 percent).

The ongoing unfavourable development in the manufacturing sector continues to dampen the momentum in remaining market services (NACE 2008, sections J to N), as the current employment situation and the sentiment indicators of the WIFO-Konjunkturtest also show. Year-on-year, value added fell by ¾ percent in both April and the first half of May (March –2 percent). In other personal services (NACE 2008, sections R to T), value added is estimated to have increased by 1¼ and 1½ percent respectively in April and in the first half of May (March +1½ percent) on the basis of price-adjusted non-cash payments in the events sector.

1 The inclusion of newly published monthly and quarterly data, which have to be met when estimating the WWWI, has led to a revision of the WWWI for GDP: February +¾ percentage points, March –¾ percentage points. On the production side, noteworthy downward revisions occurred in the remaining market services (NACE 2008, sections J to N), the goods producing sector (NACE 2008, sections A to E) and trade (NACE 2008, section G).

2 Adjustment procedures for the leap year effect in February and the calendar effect of Easter in March and April 2024 are not applicable due to the short sample period – weekly data are available from January 2019 to mid-April 2024.

Weekly Economic Activity, WWWI – Production, WWWI – Demand, WWWI (from 2007) The WWWI is under constant development; it is regularly reviewed and will be expanded with new and additional weekly data series as they become available. The WWWI is not an official quarterly estimate, forecast or similar of WIFO.

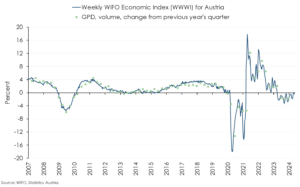

The WIFO Weekly Economic Index (WWWI) is a measure of the real economic activity of the Austrian economy on a weekly and monthly frequency. It is based on weekly, monthly and quarterly time series to estimate weekly and monthly indicators for real GDP and 18 GDP sub-aggregates (use side 8, production side 10) of the Quarterly National Accounts.

With the release for June 2022, the econometric models for the historical decompositions and for nowcasting have been converted to seasonally unadjusted time series. In addition, year-on-year growth rates are now used to estimate the models.

The WWWI estimates are (currently) updated monthly and published on the WIFO website.

Please contact