Decoupling of Trade Relations

The assessments result from a model simulation now published in a joint working paper by researchers from the Kiel Institute for the World Economy and the Austrian Institute of Economic Research (WIFO). "A trade war between Russia and the USA and its allies would hit Russia's economy hard in the long term. Although the allies are also likely to be hit hard to some extent in the short term, in the longer term they would only have to fear an annual 0.17 percent drop in economic output overall in the model-simulated case", says Alexander Sandkamp, a trade researcher at Kiel Institute and Christian Albrechts University Kiel.

The calculations were made using the KITE model (Kiel Institute Trade Policy Evaluation). The model can simulate how trade flows adjust in the long term when international supply chains are interrupted and how this affects the growth opportunities of an economy. It does not model the short-term effects of reciprocal sanctions, which usually lead to income losses on both sides. The model simulates a doubling of non-tariff trade barriers, but does not model the recently adopted sanctions against Russia.

The reason for the uneven distribution of costs lies primarily in Russia's low economic importance compared with the USA and its allies. The latter are thus more important for Russia in terms of imports and exports than vice versa: in 2020, for example, the EU was responsible for 37.3 percent of Russia's foreign trade, but only 4.8 percent of the EU's foreign trade takes place with Russia. If intra-European trade is also taken into account, Russia's share would be even lower. Import barriers imposed by the allies would hit Russia harder than export barriers.

"Sanctions usually have an economic but not a political impact in the short term. If they last for a long time and are comprehensive, their political impact can increase. The simulation results give an impression of what is at stake for both sides in the long term: after a period of adjustment in world trade, Russia will be significantly weakened, while the damage for the allies is manageable", says Gabriel Felbermayr, Director of WIFO.

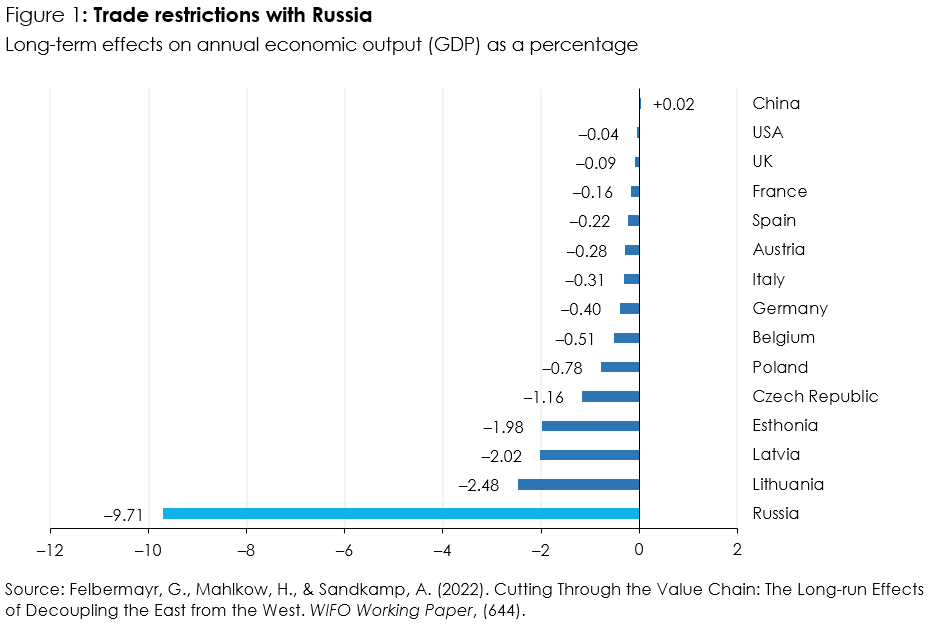

However, according to the simulation, the costs are also very unevenly distributed among the allies. Eastern European countries such as Lithuania (–2.5 percent in the modelled scenario), Latvia (–2.0 percent) and Estonia (–2.0 percent) would be hit harder in the long term. Germany and Austria would have to reckon with losses of 0.4 and 0.3 percent of annual GDP respectively, while the USA would only suffer losses of 0.04 percent. These figures show Russia's stronger economic ties with the EU.

As a result of the conflict, Russia could indeed expand its trade with other countries such as China and, in particular, export more to these countries. In 2020, just under 14.6 percent of Russian exports went to China, but only just under 2.8 percent of Chinese imports came from Russia. Even if Russia now exports more to China, the impact on China is likely to be limited. The situation is similar for Russian imports.

Thus, just under 23.7 percent of Russian imports came from China. At the same time, however, only just under 2 percent of Chinese exports went to Russia. Overall, real income in China would therefore only increase by 0.02 percent per year in the modelled scenario. In economic terms, China would therefore not be the big winner of the crisis.